Constructs an EWMA chart for a single column of individual measurements. The chart is more sensitive than a Shewhart I chart to small but persistent shifts in the process mean, at the cost of a longer reaction time to large shifts.

Usage

shewhart_ewma(

data,

value,

index = NULL,

target = NULL,

sigma = NULL,

lambda = 0.2,

L = 2.7,

steady_state = FALSE,

rules = "nelson_1_beyond_3s",

locale = getOption("shewhart.locale", "en"),

verbose = NULL

)Arguments

- data

A data frame.

- value

Tidy-eval column reference for the measurement.

- index

Optional tidy-eval column reference for the x-axis.

- target

Numeric. Process target / centre line. Defaults to

mean(value).- sigma

Numeric. Process sigma. Defaults to

MR_bar / 1.128.- lambda

Numeric in

(0, 1]. Smoothing constant. Default0.2. Smaller lambda = more memory, more sensitive to small shifts.- L

Numeric. Width of the limits in standard errors of the EWMA. Default

2.7, which combined withlambda = 0.2yieldsARL_0 ~ 370(Lucas & Saccucci 1990).- steady_state

Logical. Use asymptotic (constant) limits instead of time-varying ones?

- rules

Character vector of runs rules to flag. Defaults to Nelson 1 only — the EWMA's own limits already encode most of the diagnostic power and the higher-order Nelson rules are not designed for autocorrelated statistics.

- locale

One of

"en","pt","es","fr".- verbose

Logical. Print progress messages?

Value

A shewhart_chart object of subclass shewhart_ewma. The

augmented slot has columns .value (the original observation),

.ewma (the smoothed statistic z_i, plotted on the chart), and

the usual .center, .upper, .lower, .flag_*.

Details

By default, sigma is estimated from the moving range of value

(Wheeler 1992 convention, MR_bar / 1.128); the centre is the mean

of value. Either can be overridden via target and sigma for

Phase II monitoring against pre-calibrated values.

Limits are time-varying by default — they widen out from target

as the EWMA "warms up" — converging to the asymptotic limits as

i -> infinity. Set steady_state = TRUE to use the asymptotic

limits everywhere (commonly chosen when calibrating from a long

baseline).

References

Roberts, S. W. (1959). Control Chart Tests Based on Geometric Moving Averages. Technometrics, 1(3), 239-250. doi:10.1080/00401706.1959.10489860

Lucas, J. M., & Saccucci, M. S. (1990). Exponentially Weighted Moving Average Control Schemes: Properties and Enhancements. Technometrics, 32(1), 1-12. doi:10.1080/00401706.1990.10484583

Montgomery, D. C. (2019). Introduction to Statistical Quality Control (8th ed.). Wiley. Chapter 9.

Examples

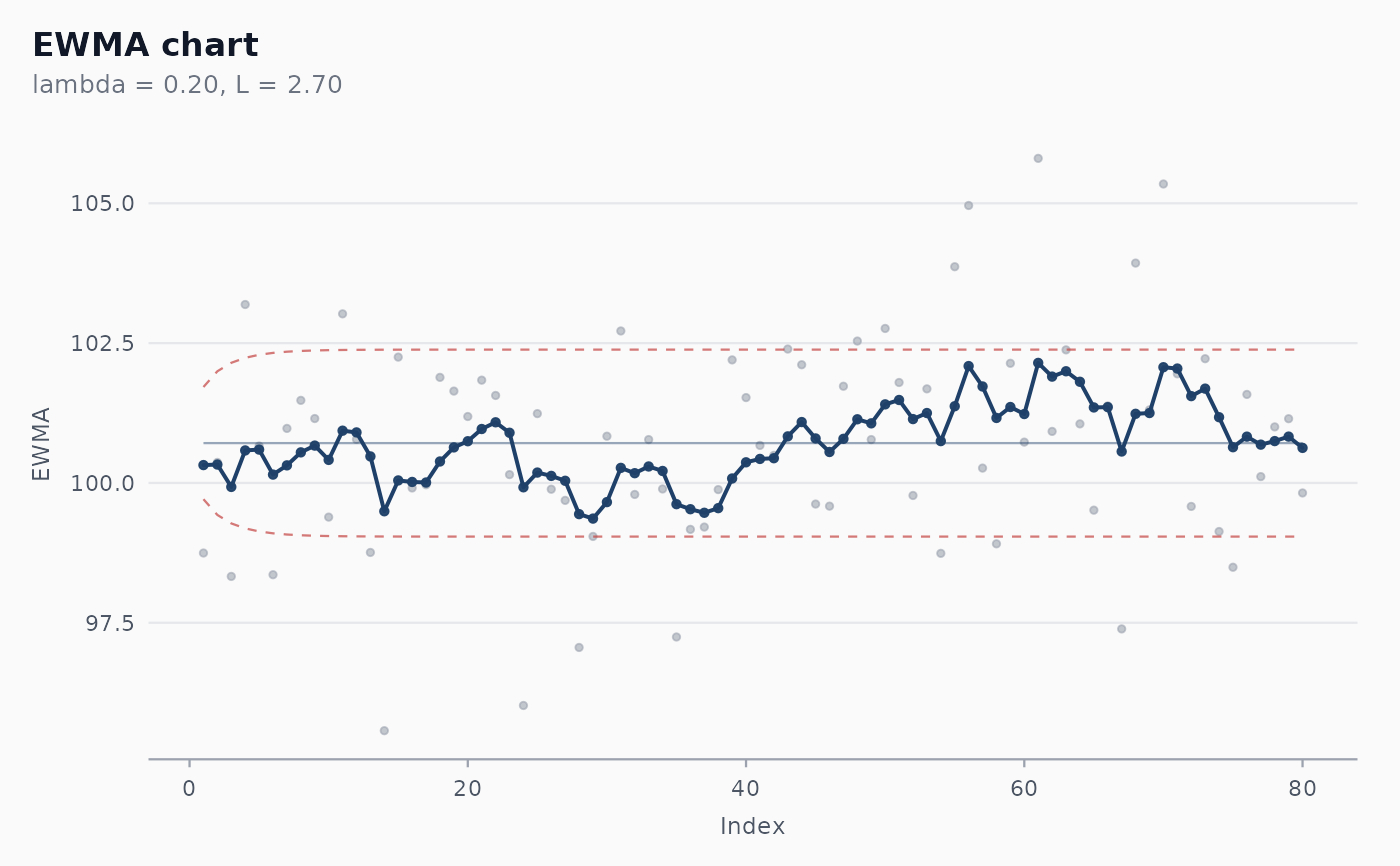

set.seed(1)

df <- data.frame(

day = 1:80,

y = c(rnorm(40, mean = 100, sd = 2),

rnorm(40, mean = 101, sd = 2)) # 0.5 sigma shift

)

fit <- shewhart_ewma(df, value = y, index = day)

print(fit)

#>

#> ── Shewhart chart ewma ─────────────────────────────────────────────────────────

#> • Observations / subgroups: 80

#> • Phase: "phase_1"

#> • Sigma estimate ("mr"): 1.857

#>

#> ── Control limits ──

#>

#> # A tibble: 3 × 3

#> chart line value

#> <chr> <chr> <dbl>

#> 1 EWMA CL 101.

#> 2 EWMA UCL_asymptotic 102.

#> 3 EWMA LCL_asymptotic 99.0

#> ── Rule violations ──

#>

#> ✔ No violations across 1 rule: "nelson_1_beyond_3s".

# \donttest{

ggplot2::autoplot(fit)

# }

# }