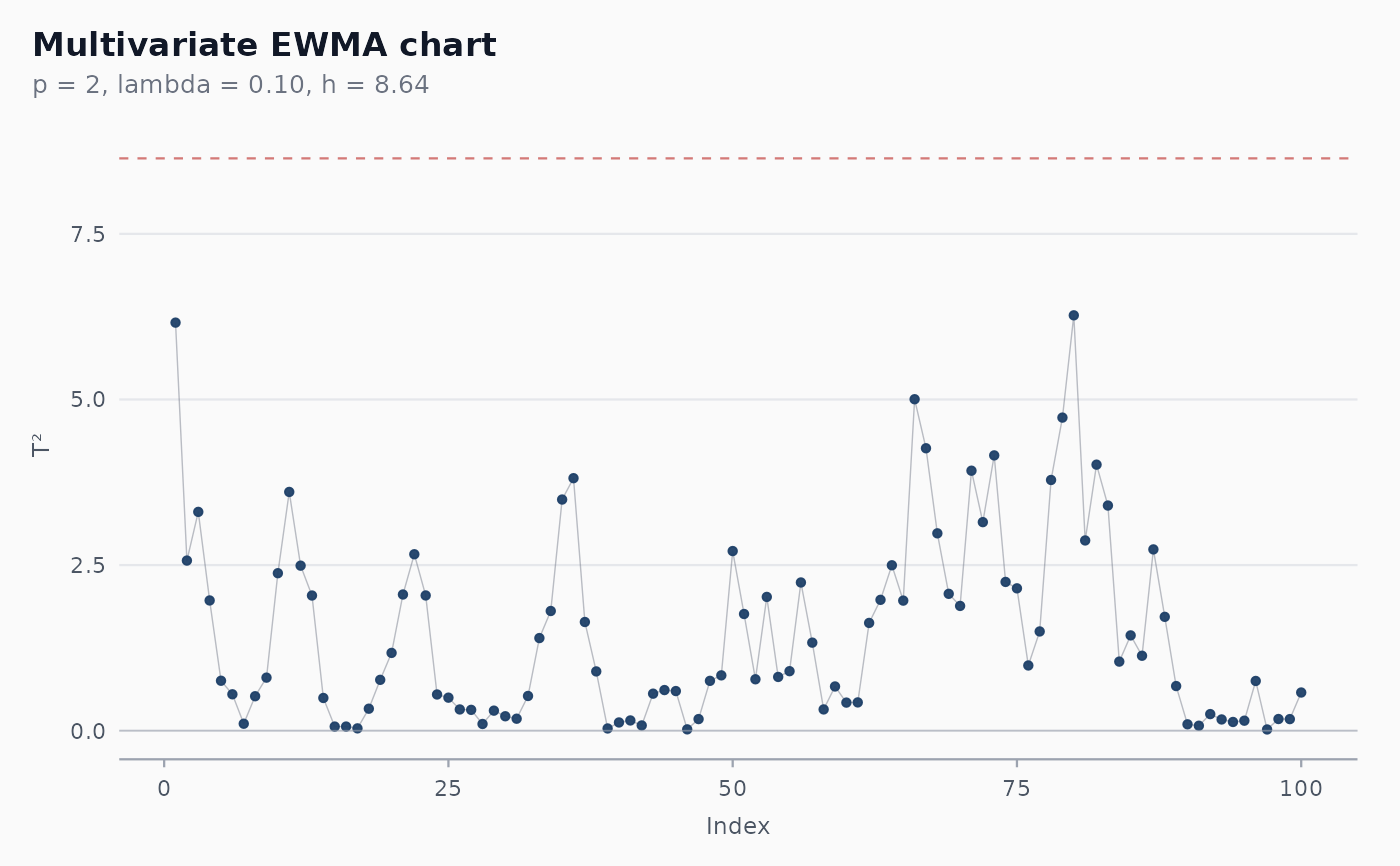

Constructs a multivariate Exponentially Weighted Moving Average

(MEWMA) chart for jointly monitoring p correlated variables.

The chart is more sensitive than the Hotelling T^2 chart to

small persistent shifts in the vector mean, in the same way the

univariate EWMA is more sensitive than a Shewhart I chart.

Usage

shewhart_mewma(

data,

vars,

index = NULL,

target = NULL,

cov = NULL,

lambda = 0.1,

h = NULL,

steady_state = FALSE,

locale = getOption("shewhart.locale", "en"),

verbose = NULL

)Arguments

- data

A data frame.

- vars

Tidy-select expression for the columns to monitor jointly. Must select at least 2 columns.

- index

Optional tidy-eval column for the x-axis.

- target

Optional length-

pnumeric vector. The in-control mean. Defaults tocolMeans(data[, vars]).- cov

Optional

p x pcovariance matrix. Defaults tocov(data[, vars]).- lambda

Smoothing constant in

(0, 1]. Default0.1.- h

Decision interval (UCL on the

T^2statistic). IfNULL, looked up in the Prabhu & Runger (1997) table forARL_0 ~ 200.- steady_state

Logical. Use the steady-state covariance

(lambda / (2 - lambda)) * Sigmaeverywhere instead of the time-varying form? DefaultFALSE.- locale

One of

"en","pt","es","fr".- verbose

Logical. Print progress messages?

Value

A shewhart_chart object of subclass shewhart_mewma.

The augmented tibble has columns .t2 (the MEWMA statistic),

.upper (the decision interval h), and .flag_signal.

Details

By default target (the in-control mean vector) and cov (the

in-control covariance) are estimated from the data. For Phase II

monitoring, supply both explicitly so the limits use the

calibration values. The decision interval h is calibrated by

lookup in the Prabhu & Runger (1997) table for ARL_0 ~ 200; if

the (lambda, p) combination is outside the tabulated range, the

user must pass h explicitly.

References

Lowry, C. A., Woodall, W. H., Champ, C. W., & Rigdon, S. E. (1992). A Multivariate Exponentially Weighted Moving Average Control Chart. Technometrics, 34(1), 46-53. doi:10.1080/00401706.1992.10485232

Prabhu, S. S., & Runger, G. C. (1997). Designing a Multivariate EWMA Control Chart. Journal of Quality Technology, 29(1), 8-15. doi:10.1080/00224065.1997.11979721

Examples

set.seed(1)

Sigma <- matrix(c(1, 0.6, 0.6, 1), 2, 2)

base <- MASS::mvrnorm(60, c(0, 0), Sigma)

shift <- MASS::mvrnorm(40, c(0.4, 0.4), Sigma) # 0.4 sigma shift

df <- data.frame(t = 1:100,

x1 = c(base[, 1], shift[, 1]),

x2 = c(base[, 2], shift[, 2]))

fit <- shewhart_mewma(df, vars = c(x1, x2), index = t,

target = c(0, 0), cov = Sigma,

lambda = 0.1)

print(fit)

#>

#> ── Shewhart chart mewma ────────────────────────────────────────────────────────

#> • Observations / subgroups: 100

#> • Phase: "phase_1"

#> • Sigma estimate ("mewma"): NA

#>

#> ── Control limits ──

#>

#> # A tibble: 1 × 3

#> chart line value

#> <chr> <chr> <dbl>

#> 1 MEWMA UCL 8.64

#> ── Rule violations ──

#>

#> ✔ No violations across 1 rule: "mewma_h".

# \donttest{

ggplot2::autoplot(fit)

# }

# }